Cases from US, the UK, India and with extra focus from Turkey

Figure 1

Developed and developing countries have different trade balance structures and dynamics. With regards to international electric and electronic related trade there is a similarity amongst many countries in terms of their trade deficit. Trade deficits pose numerous challenges to a national economy, while controlling they may have some benefits.

Piana (2006) briefly explains that a persistent trade deficit may lead to foreign debt, which if badly managed, can pave the way to a currency crisis.[1] On the other hand, trade deficits could keep prices lower, a certain extent enabling a competitive environment. As well as the monetary issues, long-lasting trade deficit has the potential to cause failure of local firms leading, so job loss due to outsourcing to other countries.[2] Concerning the speed of technological advancement, and the disproportionate balance between the cost and profit of technological and basic consumer goods, a national economy must embark on journey of understanding how to improve its own produce as well as its rules on trade to be able to cope with the trade deficit. However, Figure 1, indicates a trend for a higher deficit with total imports being double than the total exports cumulatively in the US, the UK, India and Turkey. This article will seek to analyse the effects of electronic goods on the international trade balance while especially examining the situation in the US, the UK, India and Turkey. It will also include short overview of Turkish policy regarding electric and electronics trade.

Figure 23

The trade deficit of the US rose to $45.2 billion as of November 2016.[3] Moreover, in 2016 statistics indicate that a deficit of $168 million was due to the trade of electrics and electronics (Figure 2[4]). The gap has been increasing for the last 5 years with exports only constituting 35% of the electrics and electronics trade flow (Figure 3[5]).

Figure 3

According to an article on Wall Street Journal, in 2013 electronics imports had a portion of 15.8% of the trade deficit for the US economy.[6] These numbers highlight that importing cheaper electronic goods like devices for communication and computer materials, have been causing a severe damage to the US based producers and to the nations’ trade balance. More precisely, the US growth in value of electronics has only shown a 1.76% increase between the period of 2005 and 2008. The highest loss was observed in consumer electronics with 4.22%, while the US medical & industry electronics have grown by 4.30% during this period.[7] A conclusion that can be drawn from these figures is that the American electronics sector remained weak vis-à-vis the foreign products and imports. The supply of electronics produced overseas surpassed the value of American production, especially in the areas of consumption electronics. More advanced subsectors such as medical & industry products maintained an upward trend and the national produce was able to develop in these areas. Finally, graph above, indicated that we have witnessed an upward trend in the value of American exports in recent years as a result of technological leverage against the low cost foreign products. We may speculate that the recovery of the American electronics industry after the 2008 crisis may have been the main initiative of this growth, which has shown another worrying $2 billion fall in 2015.

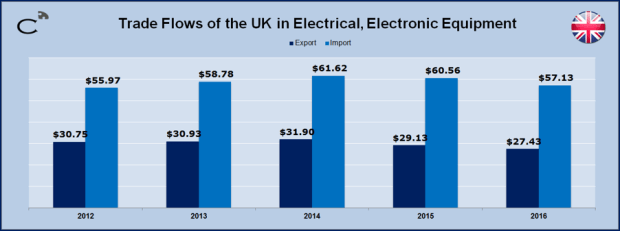

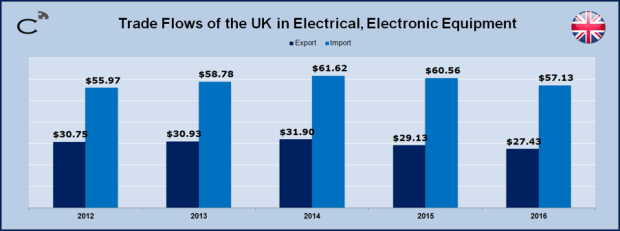

The situation for the UK is not much different. In 2015, the annual trade deficit accounted to £36.6 billion.[8] Based all exports, electronic equipment trade accounted for 8% with EU and 7% with non-EU countries, while imports constitued a bigger portion, comprising 10% with EU, and 11% with non-EU partners.[9] However, over the period of 2005 to 2008, the value of English ICT products experienced a decline of 1.34%. Of all ICT sectors, the loss in consumer electronics went up to 7.60%, while the biggest loss was experienced in office equipment with 15%. The telecommunications sub sector remained at a 2.64% growth value, while the biggest achievement was in medical & industrial products with a 7.34% growth.[10] Furthermore, the trade deficit seems to be stable at around $30 Billion for 3 years (Figure 4[11]).

Figure 4

These results are very similar to those of the US. The overall tendency of these two developed economies exhibits a loss of domestic market share to foreign goods and companies. Within the sector of electronics, the advanced material production still remains at a higher value as the necessary equipment and human capital would are still supplied more effectively by these developed economies. Following this trend, British electronics have been at a continuous fall in value. As seen in the comparative table above, in spite of the American recovery, the UK’s exports in electronics have either been devalued or remained at a halt.

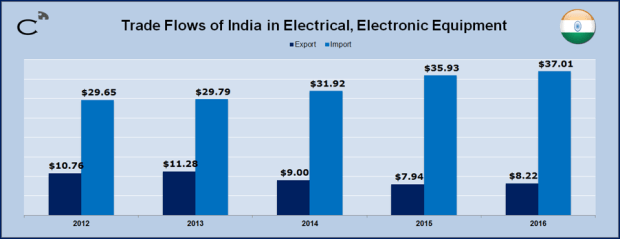

India is also another country with a sizeable trade deficit. The year-on-year trade gap has widened by 25.9% in November 2016, yielding a $13 billion deficit.[12] Although India has developed itself as a software and technology giant, with software export accounting for 91% of its ICT exports, Indian exports in ICT sector have been dwarfed by its imports with a figure of $18 billion to $1.8 billion over the course of 1997-2007.[13] Recent data indicate a greater deficit in the electrics and electronics sector, reaching $ 28.8 billion in 2016 (Figure 5[14]).

Figure 5

The growth of the ICT sector is due to the increase in the consumption levels for local or re-exported products. In the period between 2005 and 2008, Indian electronics sector experienced an annual growth in value by 19.93%, coming in 3rd place after Slovakia and Brazil.[15] This promising figure proves that Indian policy makers have been able to obtain a clear vision of future technology and communications and have affectively directed investment to these areas. Perhaps, regarding its status as a developing BRICS power, India’s progress in the software sector demonstrates an exemplary path for other developing powers to follow. Indian specialization in software and product development offers a comparative advantage to the nation’s growing economy, while opening up job opportunities for the Indian youth. As a developing economy, when compared to the examples of the UK and the US, the progress of India progress in the electronics sector demonstrates a need to trickle down the strength of the software sector to other segments of the electrics and electronics industry.

The Turkish economy yielded a trade deficit of $4.1 billion in November 2016. In 2014, Turkish exports in machinery and electronics ($25.8 billion) were dwarfed by the imports which were almost double the volume ($46.7 billion).[16] Moreover, between 2005 and 2008, which we dwelled upon in the other cases, the Turkish electronics sector remained mostly at a halt. Office equipment lost a growth value of 5.80%, while components gained 6.73% and medical & industrial products gained 3.98%. The remaining subsectors could not surpass above a percentage of 1.64%, and overall value growth was only 2.01%.[17] For a country in the league of developing economies, these figures are worrying for the economic future growth.

Following these figures, in the period of 2011 and 2016 Turkish exports have been at a steady fall in value regarding Electrics and electronics industry (Figure 6[18]).

Figure 6

Indeed, t this day Turkish policy makers seem to not prioritise the electronics sector. When compared to value growth in the same period in other developing countries like India, Korea or Slovakia (See Figure 7), the Turkish electronics sector is far behind. In addition, instead of focusing on sector improving policies Turkish officials have applied a tax raise for the import of electronic products.[19] One major issue here is in the basic mentality of protecting the domestic economy vis-à-vis the foreign competition. It is a well-known however that the import substitution methods in the 70’s left the country crippled and economically behind in comparison to the export oriented economies the South Asian countries. While at a same level of development in those years, South Asian economies managed to flourish in following decades, thanks to competitive, export oriented policies.

Figure 7

To give an example, South Korea, which was an aid receiving country, that lacked economic possibilities or opportunities only 50 years ago, has managed to become a donor country at the end of this period. South Korea’s success was due its strategic investment and incentive policy in the beginning of the 80’s, focusing especially in the areas of IT and technology.[20] Consequently, South Korea was ranked as the 5th largest export economy in 2014 and in the same year it yielded a $75 billion trade surplus.[21] Moreover, South Korea has experienced a continuous positive trade balance since 1998. The trend of continuous surplus is stable in terms of the all electrics and electronics industry( See Figure 8).

Figure 8

Mobile phones constituted a 2.7% of all exports in this period with a total value of $15.6 billion.[22] Samsung, South Korea’s technology giant, corresponds to the country’s 60% of all mobile phone exports.[23] Interpreting the data, looking at this data, we may estimate that Samsung mobile phones correspond to approximately 1.5% of the country’s total exports. This is an incredible portion of the country’s exports to hold for a single product line of a company. The creation of such a global giant was certainly a breakthrough for the South Korean economy, and is a result of its development strategy that is known to foster an internationally competitive spirit, rather than a protection oriented ‘inward-ism’.

As seen from the data and the policy choices as well, Turkey’s electronics industry should be supported and incentives must be given to stimulate the production of high value added items, rather than protective measures. This way the Turkish electronics sector may obtain a positive future and may experience steady growth. Compared to South Korean strategies, Turkish policies lack long term vision instead they concentrate on short term tax gains. Thus, Turkish consumers experience a growing increase in prices, which is not supported by secondary local products that can supply the domestic market. That is the indication of the weak policy that vitalizes a domestic technology industry.

[1] http://www.economicswebinstitute.org/glossary/tradebalance.htm

[2] https://www.thebalance.com/trade-deficit-definition-causes-effects-role-in-bop-3305898

[3] US Census Bureau, 2017

Link: https://www.census.gov/foreign-trade/data/index.html

[4] Consilience Consulting UK Elaboration with data from United Nations Statistics Division, 2017

[5] Consilience Consulting UK Elaboration with data from United Nations Statistics Division, 2017

[6] Mitchell, J. (2013). Electronics imports drive 15.8% growth in trade gap. The Wall Street Journal Eastern Edition. p. 2.

[7] Organisation for Economic Co-operation and Development (OECD), Link: https://www.oecd.org/sti/ieconomy/45576760.pdf

[8] Office for National Statistics UK, Link: https://www.ons.gov.uk/economy/nationalaccounts/balanceofpayments/bulletins/uktrade/january2016

[9] HM Revenue & Customs (HMRC) Trade Statistics Unit, Link: https://www.uktradeinfo.com/Statistics/OverseasTradeStatistics/Pages/Commodities.aspx

[10] Organisation for Economic Co-operation and Development (OECD), Link: https://www.oecd.org/sti/ieconomy/45576760.pdf

[11] Consilience Consulting UK Elaboration with data from United Nations Statistics Division, 2017

[12] Trading Economics, http://www.tradingeconomics.com/india/balance-of-trade

[13] Organisation for Economic Co-operation and Development (OECD),

Link: https://www.oecd.org/sti/ieconomy/45576760.pdf

[14] Consilience Consulting UK Elaboration with data from United Nations Statistics Division, 2017

[15] Ibid.

[16] The Observatory of Economic Complexity, Link: http://atlas.media.mit.edu/en/profile/country/tur/

[17] Organisation for Economic Co-operation and Development (OECD), Link: https://www.oecd.org/sti/ieconomy/45576760.pdf

[18] Consilience Consulting UK Elaboration with data from United Nations Statistics Division, 2017

[19] Hurriyet Daily News, Link: http://www.hurriyetdailynews.com/turkey-to-put-additional-import-tax-on-electronic-goods-minister.aspx?pageID=238&nID=84867&NewsCatID=344

[20] Planet Earth Institute, Link: http://planetearthinstitute.org.uk/south-korea-a-true-development-success-story/

[21] The Observatory of Economic Complexity, Link: http://atlas.media.mit.edu/en/profile/country/kor/

[22] The Observatory of Economic Complexity, Link: http://atlas.media.mit.edu/en/profile/country/kor/#Exports

[23] Bloomberg, Link: https://www.bloomberg.com/news/articles/2016-10-14/woes-at-giants-samsung-hyundai-weigh-on-south-korean-exports

Additionally, Turkey is the second biggest of natural gas customer after Germany, importing 55% of its gas from Russia (See Figure: 3). Turkey also accounts for nearly a quarter of food imports in Russia with Russia being the second biggest export destination for food products following Iraq (See Figure: 4). Significantly, most citrus fruits and tomatoes imported come from Turkey, an area that further developed following the EU sanctions. As a result both the previous EU sanction and current bans are already causing inflation in food prices in Russia.

Additionally, Turkey is the second biggest of natural gas customer after Germany, importing 55% of its gas from Russia (See Figure: 3). Turkey also accounts for nearly a quarter of food imports in Russia with Russia being the second biggest export destination for food products following Iraq (See Figure: 4). Significantly, most citrus fruits and tomatoes imported come from Turkey, an area that further developed following the EU sanctions. As a result both the previous EU sanction and current bans are already causing inflation in food prices in Russia. Another sector that will be strongly affected is tourism. Which is already hit by the cancellation of holiday packages and charter flights, which were the main means of transport for tourists from Russia. The effects will be mostly felt when the holiday season will start towards the summer of 2016. Turkey is the 6th most visited country in the world, hosting over 39 million tourists following Italy with over 48 million tourists with Turkey ranking 12th in tourism receipts

Another sector that will be strongly affected is tourism. Which is already hit by the cancellation of holiday packages and charter flights, which were the main means of transport for tourists from Russia. The effects will be mostly felt when the holiday season will start towards the summer of 2016. Turkey is the 6th most visited country in the world, hosting over 39 million tourists following Italy with over 48 million tourists with Turkey ranking 12th in tourism receipts income by increasing revenue made from existing arrivals. In this case Russian tourist arrivals were approximately 4.5 million in 2014

income by increasing revenue made from existing arrivals. In this case Russian tourist arrivals were approximately 4.5 million in 2014